Your Roadmap to Accounts Receivable Financing

For many small and mid-sized businesses, cash flow isn’t a revenue problem, it’s a timing problem. Net-30, net-60, or net-90 payment terms are standard in B2B commerce, but the bills that come due in the meantime don’t wait.

Accounts receivable financing exists to close that gap. Rather than waiting for clients to pay on their own schedule, you draw against a revolving credit line secured by your outstanding invoices. As those invoices clear, you repay what you drew, and the line replenishes and stays ready for the next cycle. It’s a structure built around the way cash actually flows through a B2B business.

If you’re considering AR financing for the first time, or you’ve heard about it and want to understand what the process actually looks like, here is what you need to know before you get started.

Who AR Financing Is Built For

AR financing is designed for businesses that sell to other businesses on credit terms. Manufacturers, distributors, staffing companies, logistics providers, healthcare businesses, and wholesale operations are common users. The common thread is a consistent pattern of B2B invoicing with clients who are creditworthy, even if they’re slow to pay.

This is not a product for businesses that collect payment at the point of sale or that deal primarily with individual consumers. The collateral behind the credit line is your outstanding invoices, and for that collateral to have value, those invoices need to represent real obligations from clients with the financial standing to pay them.

If your business has a growing book of B2B receivables and you find yourself regularly waiting on cash that’s technically already earned, you’re a strong candidate.

What Lenders Are Actually Looking At

A common misconception about AR financing is that approval hinges primarily on your own business credit or financial history. It doesn’t. The primary underwriting lens is the quality of your receivables, which means the creditworthiness of the clients who owe you money and the age and health of your outstanding invoices.

This is one of the reasons AR financing is accessible to businesses that might not qualify for a traditional bank loan. A newer business with a short credit history can still access a meaningful credit line if it invoices established, creditworthy clients.

Lenders will also look at your overall business financials, including income statements, a balance sheet, and tax returns. They want to understand the business context around your receivables. Clean, organized books accelerate the process considerably.

The Importance of Industry Experience in a Lender

Not every AR financing lender operates the same way, and industry experience matters more than many borrowers realize. Healthcare receivables come with compliance considerations and reimbursement cycles that differ from commercial invoicing. Staffing companies operate with weekly payroll cycles and specific client structures. Apparel businesses deal with seasonal concentration and retailer-specific terms. A lender who understands your industry will evaluate your receivables more accurately and structure your facility in a way that fits how your business actually operates.

Our team at CapitalNetwork has longstanding relationships with lenders who have experience in many different sectors and industries. We can connect you with a lender who has financed businesses like yours before and will ask the right questions to make faster decisions.

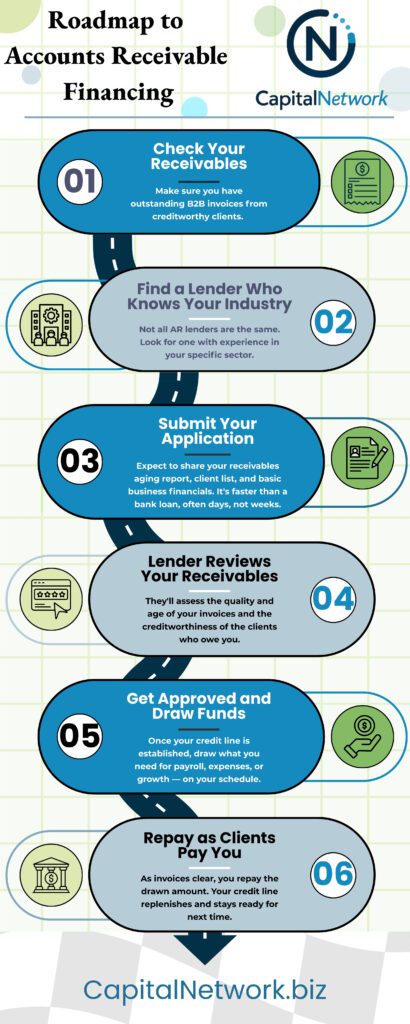

What the Process Looks Like

One of the most consistent things business owners report after going through the AR financing process for the first time is that it was faster and less invasive than they expected. Unlike a traditional bank loan, which can take weeks or months and require extensive documentation, AR financing decisions are typically made in days.

You’ll start by pulling together the documents a lender will need, including a receivables aging report that shows outstanding invoices by customer and age, a list of your major clients, recent financial statements, and basic business information. The aging report is particularly important because it gives the lender a clear picture of the receivables that will serve as collateral for the facility.

Once the lender reviews your receivables and approves your application, a credit line is established. From that point forward, you draw funds as you need them, whether for payroll, inventory, operating expenses, or a growth investment, and repay as your clients pay their invoices. The revolving structure means the line stays available and rebuilds with each repayment cycle.

What AR Financing Is Not

It’s worth being clear about a few things AR financing doesn’t do, because misunderstanding the product leads to mismatched expectations.

AR financing is not a way to address pre-shipment costs. If your challenge is funding production, purchasing raw materials, or paying suppliers before goods are delivered, purchase order financing is a better-suited tool. AR financing picks up where PO financing leaves off, once goods are shipped and invoices are issued.

It is also not factoring, though the two are frequently confused. With factoring, you sell your invoices outright to a third party, who then collects from your clients directly.

With AR financing, you retain ownership of your invoices, continue managing your own collections, and your clients are never notified that a financing facility is in place. The lender holds the receivables as collateral, not as purchased assets.

Finally, AR financing is not designed for businesses without an established invoicing history. If your business is pre-revenue or just beginning to generate invoices, there isn’t yet a receivables base to build a financing decision on.

AR financing a product for businesses that are already operating and billing, even if they’re still early in their growth trajectory.

How to Know You’re Ready

The clearest signal that a business is ready to explore AR financing is a growing gap between invoiced revenue and available cash. If you find yourself turning down new work because you don’t have the working capital to staff up or fulfill orders, if payroll is a source of stress despite strong sales, or if you’re regularly waiting 45 to 90 days for payments that should have arrived sooner, those are signs that your receivables could be working harder for you.

For more information, contact us, and we’ll let you know if AR financing is right for your business.

Latest Blogs

-

The Pros and Cons of AR Financing

AR financing gives B2B businesses a way to convert outstanding invoices into working capital without waiting on customer payment cycles. Like any financing product, it comes with advantages and trade-offs. Understanding both sides of the product helps a business decide whether it fits the situation at hand. What Is AR Financing Accounts receivable financing is…

-

Industry Spotlight: Alternative Financing for Medical Equipment Companies

Companies that manufacture, distribute, or sell medical instruments and apparatus have customers like hospitals, surgical centers, diagnostic labs, and physician groups, that are creditworthy institutions with the resources to pay their bills. Unfortunately, healthcare procurement departments operate on extended payment cycles, and a medical instruments company waiting on net-60 or net-90 terms from a hospital…

-

Tips for Quick Funding for Your Small Business

Cash flow gaps in small businesses often arrive without warning. Maybe a large customer pays late, a piece of equipment breaks down, or a new contract requires upfront investment before the first invoice goes out. When a business needs cash fast, the options available to it depend on the type of business, the assets it…

-

Industry Spotlight: Alternative Financing for Engineering Services Firms

Engineering services firms occupy a position in the project economy that looks profitable on paper and feels tight in the bank account. Civil engineers, structural engineers, MEP consultants, and specialty design firms bill for expertise rather than materials, which means their primary cost is payroll, and payroll has to be funded weeks or months before…