The Pros and Cons of Invoice Discounting

Understanding how invoice discounting works, what it costs, and whether it fits your business.

For business owners who sell to other businesses on credit terms, waiting to get paid is one of the defining frustrations of running the company. Invoice discounting is one of the tools designed to solve the problem that 30 to 90 day terms present, and it’s worth understanding before deciding whether it belongs in your financing toolkit.

What Is Invoice Discounting?

Invoice discounting is a form of short-term borrowing in which a business uses its outstanding invoices as collateral for an advance from a finance provider. Rather than waiting for clients to pay, the business receives a percentage of the invoice value upfront, typically somewhere between 75 and 95 percent, and then repays that advance plus a fee once the client pays the original invoice.

Invoice discounting is a loan, not a sale. You retain ownership of your invoices, you continue managing your own collections, and your clients are generally not aware that any financing arrangement is in place. The finance provider is a silent participant, holding your receivables as security while you keep the client relationship fully intact.

This distinguishes invoice discounting from invoice factoring, which works differently in important ways. With factoring, you sell your invoices outright to a third party, who then contacts your clients directly to collect payment. Factoring provides more upfront support for businesses without their own collections processes, but it removes the confidentiality and means your clients know a financing company is involved. Invoice discounting keeps everything in-house and out of sight.

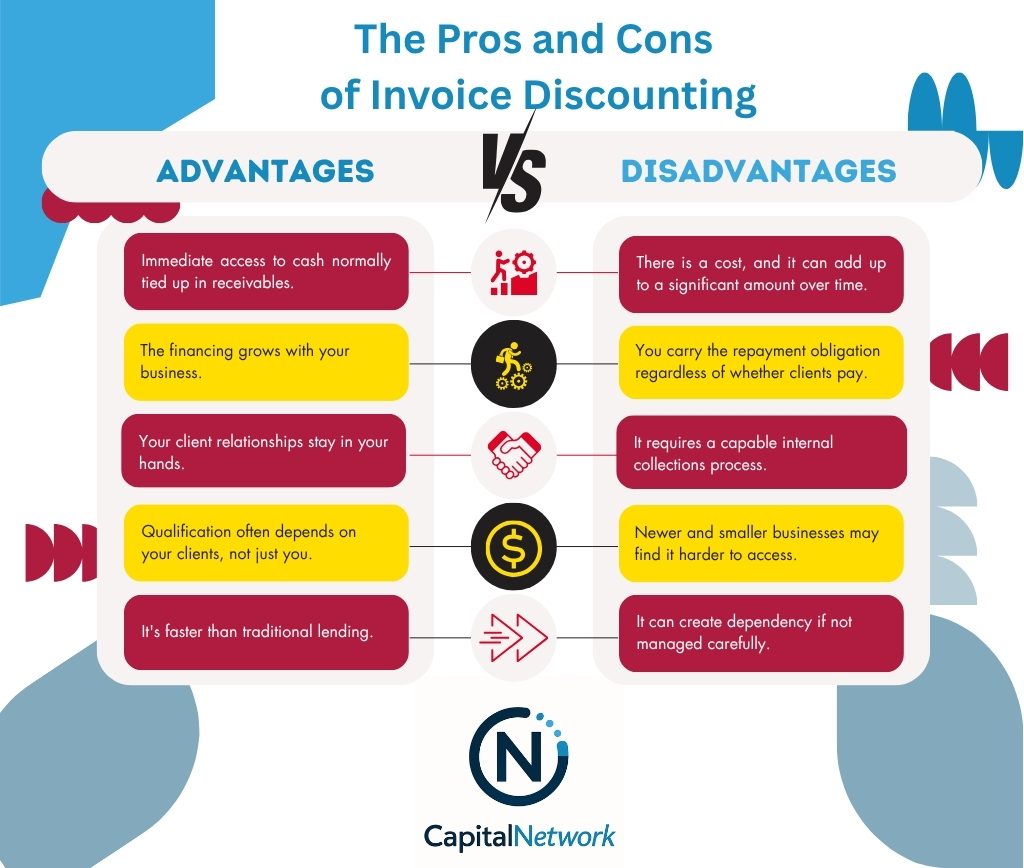

The Advantages

- Immediate access to cash tied up in receivables. The most direct benefit of invoice discounting is speed. Rather than waiting weeks or months for payment, you can access most of the invoice value within a day or two of submitting it.

- The financing grows with your business. One of the more appealing structural features of invoice discounting is that your available credit scales naturally with your revenue. As you issue more invoices, your access to working capital increases.

- Your client relationships stay in your hands. Because invoice discounting is confidential in most arrangements, your clients continue dealing only with you. They pay you directly on the original invoice terms, and they have no visibility into the financing structure behind the scenes.

- Qualification often depends on your clients, not just you. Traditional bank financing leans heavily on your business credit history, your assets, and your time in operation. Invoice discounting lenders place significant weight on the creditworthiness of the clients who owe you money.

- It’s faster than traditional lending. The application process for invoice discounting is typically far less involved than applying for a bank loan. Because the collateral is your existing invoices rather than physical assets, and because the underwriting centers on your receivables ledger, approvals tend to move in days rather than weeks or months.

Rather than waiting weeks or months for payment, you can access most of the invoice value within a day or two of submitting it.

The Disadvantages

- There is a cost, and it adds up. Invoice discounting is not free, and the fees can meaningfully reduce the net value of your invoices over time. Providers typically charge a combination of a service fee and a discount fee based on the size and age of the invoices being financed.

- You carry the repayment obligation regardless of whether clients pay. Since invoice discounting is structured as a loan rather than a sale, the borrowing obligation stays with you. If a client pays late or doesn’t pay at all, you are still responsible for repaying the advance.

- It requires a capable internal collections process. Since you retain responsibility for collecting from your clients, you need the systems and capacity to manage that effectively. Businesses that are already struggling to chase overdue invoices don’t solve that problem by adding invoice discounting.

- Newer and smaller businesses may find it harder to access. Lenders in this space tend to prefer businesses with an established track record of invoicing, a diverse client base, and a history of reliable collections. A newer business or one that generates a small number of high-value invoices may face stricter eligibility requirements, higher fees, or limited access to the product.

- It can create dependency if not managed carefully. Because invoice discounting makes it easy to access cash on demand, some businesses gradually shift from using it strategically to relying on it as a default operating mechanism. If the underlying business has structural cash flow problems, invoice discounting delays the reckoning without fixing it.

- It doesn’t cover pre-invoice needs. Invoice discounting only works once an invoice exists. It does nothing for the period before goods are shipped or services are delivered, when you may need capital to fulfill orders in the first place.

Who It Works Best For

Invoice discounting is generally most effective for businesses that have been operating for at least a year or two, invoice other businesses regularly on standard credit terms, and have reliable clients with a history of paying. Manufacturing companies, oil and energy companies, distributors, staffing businesses, and service firms with predictable B2B invoicing patterns tend to be the strongest candidates.

It is less well-suited to businesses that primarily serve individual consumers, collect payment at the point of sale, have a very small number of clients representing concentrated credit risk, or are so early in their development that they don’t yet have an established invoicing history to support a facility.

Comparing Your Options

Invoice discounting is one of several tools available for addressing the gap between invoicing and getting paid. AR financing works on a similar principle, using receivables as collateral for a revolving credit line, and is worth comparing directly. Invoice factoring offers more support but less confidentiality. A business line of credit provides more flexible use of funds but is underwritten based on overall business creditworthiness rather than specific receivables. For pre-shipment capital needs, purchase order financing fills a gap that invoice-based tools cannot.

The right choice depends on the structure of your business, the quality of your client base, how you manage collections, and what you actually need the capital for. Invoice discounting is a powerful and legitimate tool for the right business in the right situation. The work is in determining honestly whether your business is in that situation.

Latest Blogs

-

The Pros and Cons of AR Financing

AR financing gives B2B businesses a way to convert outstanding invoices into working capital without waiting on customer payment cycles. Like any financing product, it comes with advantages and trade-offs. Understanding both sides of the product helps a business decide whether it fits the situation at hand. What Is AR Financing Accounts receivable financing is…

-

Industry Spotlight: Alternative Financing for Medical Equipment Companies

Companies that manufacture, distribute, or sell medical instruments and apparatus have customers like hospitals, surgical centers, diagnostic labs, and physician groups, that are creditworthy institutions with the resources to pay their bills. Unfortunately, healthcare procurement departments operate on extended payment cycles, and a medical instruments company waiting on net-60 or net-90 terms from a hospital…

-

Tips for Quick Funding for Your Small Business

Cash flow gaps in small businesses often arrive without warning. Maybe a large customer pays late, a piece of equipment breaks down, or a new contract requires upfront investment before the first invoice goes out. When a business needs cash fast, the options available to it depend on the type of business, the assets it…

-

Industry Spotlight: Alternative Financing for Engineering Services Firms

Engineering services firms occupy a position in the project economy that looks profitable on paper and feels tight in the bank account. Civil engineers, structural engineers, MEP consultants, and specialty design firms bill for expertise rather than materials, which means their primary cost is payroll, and payroll has to be funded weeks or months before…